About Senior Home Care

Seniors who would like to continue living independently, but who are also in need of additional help with their healthcare may benefit from home healthcare services. A range of home healthcare services is available depending on the requirements of individuals, and home healthcare providers can be hired as necessary, whether on a full-time or part-time basis. Home healthcare providers can help with tasks such as bathing, grooming, dressing, and mobility needs, or they may help with the administration of medications or the performing of basic medical tasks. These services can range from extensive in-home medical care (home health care) or just help around the house and personal assistance (in-home care).

Top Cities for Home Care in the US

- Houston, TX

- Miami, FL

- Dallas, TX

- Columbus, OH

- Chicago, IL

- Los Angeles, CA

- Las Vegas, NV

- Southfield, MI

- San Antonio, TX

- Glendale, CA

- Tampa, FL

- El Paso, TX

- Garland, TX

- Mcallen, TX

- Arlington, TX

- Sugar Land, TX

- Mesquite, TX

- Oklahoma City, OK

- Stafford, TX

- Phoenix, AZ

- Burbank, CA

- Cincinnati, OH

- Laredo, TX

- Jacksonville, FL

- Skokie, IL

- Denver, CO

- Austin, TX

- Grand Prairie, TX

- Farmington Hills, MI

- Indianapolis, IN

More About Senior Home Care

Home care services are ideal for seniors who want to live independently in their own home but need help with daily living activities or medical care. You can work with the home health agency to customize the type, frequency and level of care based on the needs of the individual.

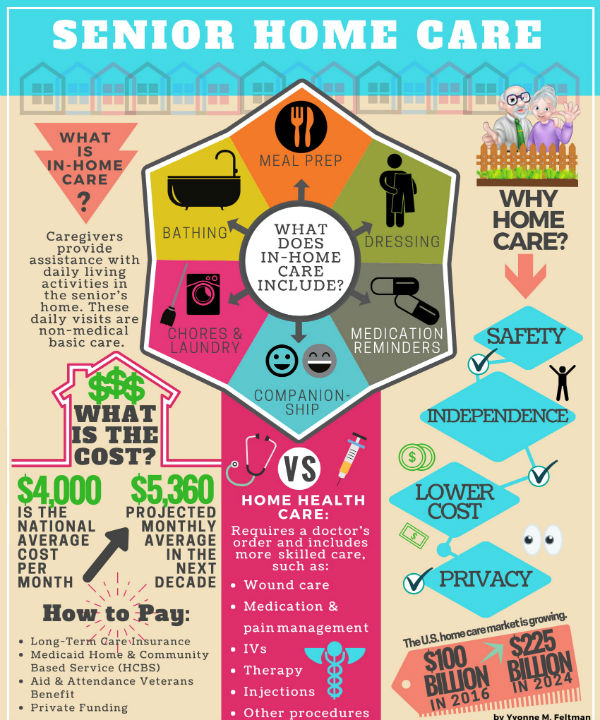

What's the Difference Between In-Home Care and Home Health Care?

Although these terms are often used interchangeably and can be provided by the same agency, there are major differences.

Home health care offers medically-based help such as injections, IVs, wound care, medication and pain management, therapy and other medical procedures. Home health care requires a written order from a doctor, while in-home care does not. Home health care is like the care that one would receive in a nursing home or skilled nursing facility and is typically less expensive. Medicare covers home health care, but it does not typically cover in-home care.

In-home care helps with daily living activities that are non-medical in nature. Typically, in-home visits happen several times per week for less than eight hours at a time. Services may include meal preparation, medication reminders, light housekeeping and chores, dressing and grooming, help with mobility, and general companionship. Some agencies offer enrichment programs tailored to each client. For example, an enrichment plan might include playing word games, painting, taking walks and attending church with her caregiver.

How Do In-Home Care and Home Health Care Work Together?

Often, home health care and in-home care are used in conjunction with one another to provide a solid regimen of care for the elderly client. For instance, a home health care nurse can change medications for the elder, while an in-home caregiver can help seniors to remember to take their medications. While an in-home caregiver can observe independent therapy exercises done by the resident and report to the physical therapist, the therapy program must be administered by the home health therapist first.

Home Care vs. Assisted Living

Home care can provide a cost-effective alternative to assisted living and allow the elderly person to remain in their home, which studies suggest contributes greatly to improved mental health. The saying "there's no place like home" holds true. Preference, abilities and cost are determining factors when choosing the right care. If your loved one requires 24/7 care, assisted living may be the best choice. However, if they only require a few hours each day of assistance, home care can cost significantly less. Most elderly home care services require a minimum of four hours, so the minimum cost is $76 per day. In contrast, According to a survey conducted by CareScout in June 2017, the national average cost per month for a private one-bedroom in an assisted living facility was $3,750.

What is Included with Home Care and Home Health Care

The types of care will overlap depending on the needs of each individual, but there are generally three types of care, which correspond to the training and education of the provider.

Licensed Medical Professional Care

Working with physicians, case managers and family members, this type of home care is administered under the care of registered nurses, therapists, medical social workers and aides. Clients patients benefit from high-quality, skilled, reliable and efficient care while enjoying the relative independence of home. Services provided may include:

- Skilled nursing services

- Administration of medications, including injections

- Medical tests

- Monitoring of health status

- Pain management

- Rehabilitation

- Wound care

Non-Medical Paraprofessional Care

Non-medical paraprofessionals include home health aides, personal care attendants, homemakers and companions. Home health aides provide hands-on care and assistance to with activities of daily living (commonly referred to as ADLs). These include:

- Bathing

- Dressing

- Feeding

- Toileting

- Grooming

- Oral Care

- Walking or using a wheelchair

They also assist with instrumental activities of daily living, which expand on the basics noted above. These include:

- Housekeeping

- Laundry

- Change linens

- General shopping

- Transportation

- Meal preparation

- Managing money

- Medication management

Dementia Care

This type of care is not very different from the above; however, dementia home caregivers have the proper training to handle the symptoms of this progressive disease and ensure your loved one's safety and quality of life. You'll want to find a provider with experience and education that includes one or more certifications in Alzheimer's or memory care.

Types of Home Care Agencies

There are four different types of home care agencies. Understanding each type will help you decide what works best for your senior loved one.

Medicare Certified Home Health Agencies

When Medicare patients receive home care, Medicare will only pay if a Certified Home Health Agency (CHHA) provides the services. Be aware that the doctor might order different services, or more frequent services, than Medicare pays for. Ask your provider whether you would need to pay for any of the services he or she wants you to have. To qualify, your doctor must certify that all the following are true:

- You are a Medicare beneficiary under a doctor's care.

- You are homebound (unable to travel outside the home without assistance).

- You need at skilled nursing care and/or physical, occupational, or speech therapy, according to Medicare restrictions and guidelines

You can find a list of all home health agencies that have been registered with Medicare on data.medicare.gov. The list includes addresses, phone numbers, and quality measure ratings for each agency.

State Licensed Home Health Agencies

Licensing for home health agencies is regulated state-by-state. The level of oversight can vary greatly. When states do not issue special licenses, the agencies only need standard business licenses for legal operation. Therefore, it's important to search for state regulations so you can better understand what licenses are required and how they're monitored. Visit the state's department of health website for information.

Non-Medical Care Agencies

If you're seeking assistance with daily living and do not need medical care, aside from medication reminders, non-medical care agencies are ideal. However, these are not covered by public or private insurance. They are also not regulated by the state or federal government, so you'll need to vet them through organizations like the Better Business Bureau.

Home Care Employment Agencies

Home care employment agencies give referrals to people seeking home care nurses and health aides. Clients may contact, hire and pay caregivers directly. If you decide to hire a caregiver independently, you should consult with a lawyer and accountant to make sure you meet all obligations. If you treat them as an employee, you are responsible for paying taxes, Social Security and Medicare, income tax withholding and unemployment tax. If you treat them as a contractor, the caregiver is responsible for their own taxes, but you'll need to file a 1099 form with the IRS. You'll also want to consider what hourly rate to pay, whether to provide paid vacation time/holidays and how to handle back up if they are sick or away.

How Much Does Senior Home Care Cost?

According to a survey conducted by CareScout in June 2017, the national average cost per month for in-home care was about $4,000. This figure is expected to rise to over $5,360 in the next ten years.

Home health care, also referred to as a home health aide, costs about $4,100 per month according to the CareScout survey, and it is projected to rise to over $5,500 over the next decade. Home health care and in-home care are not inexpensive, but they cost significantly less than care in a nursing home or skilled nursing facility (SNF).

How Can I Pay for Senior In-Home Care

Home care expenses are most frequently paid for out-of-pocket or by a combination of other methods such as Social Security, pensions, Veterans benefits, insurance, home equity, and various savings.

Long-Term Care Insurance

Long-term care insurance is a policy that is purchased through a private insurance company. Like health insurance policies, the price varies greatly depending on age, general health and amount of coverage. Coverage could be denied for people with pre-existing conditions such as Alzheimer's disease or Parkinson's disease. Not all insurance will deny based on these conditions, so it is important to explore different insurance companies.

Medicare

Medicare is a federal government program for those 65 or older with low income and limited assets. It generally does not pay for in-home care, but it will cover home health aide services such as therapy services (occupational, speech, physical) and skilled nursing care. Home health services may also include medical social services, medical supplies for use at home, durable medical equipment, or injectable osteoporosis drugs. That said, Medicare does not pay for around the clock health aide care, meals or personal assistance.

Medicaid

Medicaid is a Federal and State health insurance program for those with low income and limited assets. Administration of the program varies by state, according to the Centers for Medicare and Medicaid Services (CMS). The Medicaid home and community-based service (HCBS) waiver program provides general health coverage and coverage for certain services to help seniors stay at home or in a community-based setting. Since Medicare only covers home health care if certain criteria are met, such as being homebound and needing skilled care, additional services may still be needed.

Medicaid can be used to supplement the amount and kind of services received. If Medicare's requirements for home care aren't met, eligibility for a Medicaid HCBS waiver program is still possible. According to MedicareInteractive.org, services covered through an HCBS waiver program vary by state and may include:

- Personal care, homemaker tasks and chores

- Skilled nursing and therapy care

- Home modifications

- Adult daycare

- Respite care

- Case management

Aid and Attendance Benefit for Veterans

According to the VA website, the Aid and Attendance (A&A) benefit is a special benefit for war era veterans and their surviving spouses. It is a tax-free benefit designed to provide financial assistance to help cover the cost of long-term care in the home, board and care, assisted living communities, and private-pay nursing homes. This benefit is for those who are mentally or physically incapacitated or require the regular attendance of another person or caregiver in at least two of the daily activities of living. To learn more about the eligibility requirements and to apply for these veteran benefits visit VeteransAid.org online.

Life Insurance

Some life insurance policies may provide options to help pay for home health care. These options greatly depend on the type of life insurance policy so it's best to discuss with an insurance broker or financial advisor.

- Life Settlement - You can sell your life insurance policy to a third party for market value and use the proceeds to fund home health care.

- Surrender Policy - You give up ownership and the death benefit. If the policy has accumulated cash, the insurance company writes you a check for the full amount of cash value, which is often taxed.

- Policy Loan - You can take a loan from your life insurance policy, which means you won't pay taxes. However, you can't take it all or the policy will lapse.

- 1035 transaction - This allows you to exchange cash value tax-free from an existing life insurance policy into a new life insurance policy that provides home health care benefits.

Reverse Mortgage Loans

The Home Equity Conversion Mortgage (HECM) is a reverse mortgage that seniors take against their home's equity. Insured by the federal government, it is only accessible via lenders approved by the Federal Housing Administration (FHA). Once finalized, the lender makes payments in a single lump sum, monthly installments, or as a line of credit. The loan does not have to be paid back until the last borrower passes away or moves from the home for one full year. The home is usually sold, and the lender is paid back the full loan amount plus interest.

Private Funding

In situations when costs aren't covered through other means, paying via private funds is an option. Sources of private funds for a home health aide or in-home care include retirement accounts and 401Ks, savings accounts, annuities and insurance plans (including life settlements), trusts and stock market investments. Home equity and bridge loans can also be used when increasing care services. Social Security can also be used as a payment source for those who need care services inside their home.

Assessing Non-Medical Home Care Needs

If your loved one requires medical care, the type of care will be determined together with their health care team. However, since you are more familiar with your senior's daily living routine, you'll need to assess if they also need non-medical assistance. Here is a list to think about what might be appropriate. This is an important task prior to contacting agencies, so you know exactly what you need.

- Bedroom related tasks such as getting in/out of bed, making the bed, changing linens

- Bathroom related tasks such as help with bathing, toileting, grooming, and bathroom cleaning

- Personal care tasks such as dressing, transferring, walking

- Eating related tasks such as planning menus, preparing and serving meals, help with feeding, washing dishes, cleaning kitchen

- Other household tasks such as laundry, taking out the trash, dusting, tidying up, vacuuming, sweeping, mopping or yard work

- Shopping related tasks such as preparing a list, running errands, grocery shopping and putting away items

- Transportation to social activities or doctor appointments

- Social activities like reading to your loved one, playing games or conversation

- Money related activities like managing checkbook and paying bills

- Medication related activities like taking to the pharmacy and medication reminders

Evaluating Home Care Agencies

Now that you have a good idea of what you're looking for, use these questions to help screen home health agencies.

- Is the agency Medicare certified? You must use a Medicare Certified Home Health Agency (CHHA) to be eligible for Medicare coverage for home care.

- Is the agency licensed by the state? Not all states have licenses for home care agencies. If your state does regulate home care providers, choosing one with the proper licensing will give a higher assurance of quality.

- Does the agency carry insurance? Choose an agency that has its caregivers bonded and insured and carries professional liability insurance and general liability insurance.

- How will the agency assess needs? Most agencies begin by sending someone to make an initial assessment of needs. Although you may have performed a needs assessment for the elder in your care, you should ask the agency how it determines the appropriate level of services and if the assessment will be conducted by a medical professional.

- What services do they provide? Home care agencies may provide medical services, non-medical services or both. Confirm that all your desired services are available. For example, not every state-licensed center has an RN on call 24/7. Sometimes an aide who helps with bathing and dressing can't cook meals, or someone who cleans and does shopping isn't licensed to drive with the elder in the car. Aides also may not be able to administer medications.

- What is the training and experience of the caregivers? Does the agency require that its caregivers participate in a continuing education program? Ask if the caregivers are trained to identify and report changes in service needs and health conditions. Be sure to ask if emergency training is included in employee orientation. Do they know the Heimlich maneuver and CPR?

- Do you have caregivers who specialize in certain areas? Do the caregivers have experience or receive special training in the type of care that is needed, such as Alzheimer's care? Do they have training with assistive technology, such as a Hoyer lift?

- How do you ensure a good fit between client and caregiver and that there's continuity of care? Ask them to explain their procedure for matching clients with caregivers. Can the agency reasonably ensure that the same caregiver(s) will provide the home care services each week? How long do caregivers stay with the agency? If a substitute caregiver is sent, when does the agency provide notice to the client?

- How thorough are the agency's background checks? Effectively vetting a potential employee involves talking with their previous employer and other references. They should also get a full criminal background check to be aware of any felonies, misdemeanors and driving violations.

- How can the agency be paid? If you will be paying for service, compare the billing process and payment plans offered by different agencies. Ask if there are additional costs, such as fees or deposits, not included in the price quoted. Will you have to pay extra for holidays and weekends?

Additional Home Care and Home Health Care Resources

- How to Pay for Home Health Care

- How to Hire the Best Caregiver for a Senior in Need

- Senior Home Care - Registered Nurses vs. Home Caregivers

- How to Screen a Home Health Care Provider

- Dispelling Common Myths About Home Care

- What is Home Health Care?

- Examining Homecare Options: Continued Independence

Top Articles in Home Care

View All

Hiring a Senior Caregiver

Hiring a caregiver for a senior with a debilitating condition is an important part of a care solution for someone in need. However, finding the perfect person - one who will provide professional, compassionate care for your senior in need - can be a difficult and intimidating process for a variety...More

Read More

How to Screen a Home Health Care Provider

There are many families who ultimately choose to hire a home health care professional to help care for a senior loved one and provide them with the attention they need in order to live safely in their own homes. A home health care provider can be a powerful ally in any senior's care plan. However, i...More

Read More

What is Home Health Care?

Home is where the heart is - and it's where your loved one wants to be. For years he's built a life inside these walls, forging memories and experiences. Leaving them behind is impossible, even as his health begins to deteriorate and his need for full-time care grows. He wants to maintain a sense of...More

Read More Your Information is Processing

Your Information is Processing